By: Stash Graham

The monthly BSL Employment Report generates a surprising amount of discussion by investors and analysts. do receive other leading indicators (more on this shortly) that do not generate nearly as much coverage on financial media outlets.

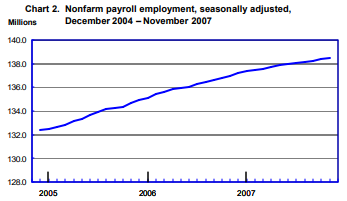

The headline number was 236,000 non-farm payroll jobs created for the month of April. This was a pleasant surprise as consensus was expecting less (190,000), but the headline resultdoes not provide any material information about the future of the American household. The chart below is the nonfarm payroll employment figures for the United States covering December 2004 to November 2007. Studying the chart, the employment growth is impressive, but does not indicate the worst recession in a generation was going to start 60 days later.

That said, the April Employment Report provided an ingredient in the employment report that analysts and investors have long waited for: Productivity. The lack of productivity has long been missing and has perplexed our financial and banking industry leaders like Federal Reserve Chairman Jerome Powell.

When labor-cost pressures increase and businesses have the will and capital to act, productivity grows. First quarter non-farm productivity expanded by 3.6%, well above the consensus expectation of 2.2%. Average Hourly Earnings and the Employment Cost Index are running close to post-’Great Recession’ highs. If we see continued moderate growth in business fixed investment, productivity should continue to improve. Bringing this all together, productivity is not a leading indicator, but it does provide investors comfort that the next couple of monthly employment reports should not provide any negative surprises.